IVL challengers face a challenge: 90% physicians plan to stick with Shockwave

Recent acquisitions suggest the peripheral IVL space is moving from a one-player market to a four-way race* within the next 18 months. But latest survey data from medintel suggests ~90% physicians plan to stay on Shockwave, despite new devices from large players becoming available.

The data

medintel surveyed 311 vascular surgeons and interventional radiologists across the US and EU in Q1 2026 — independent, non-commissioned research via the Mr Doctor Network panel.

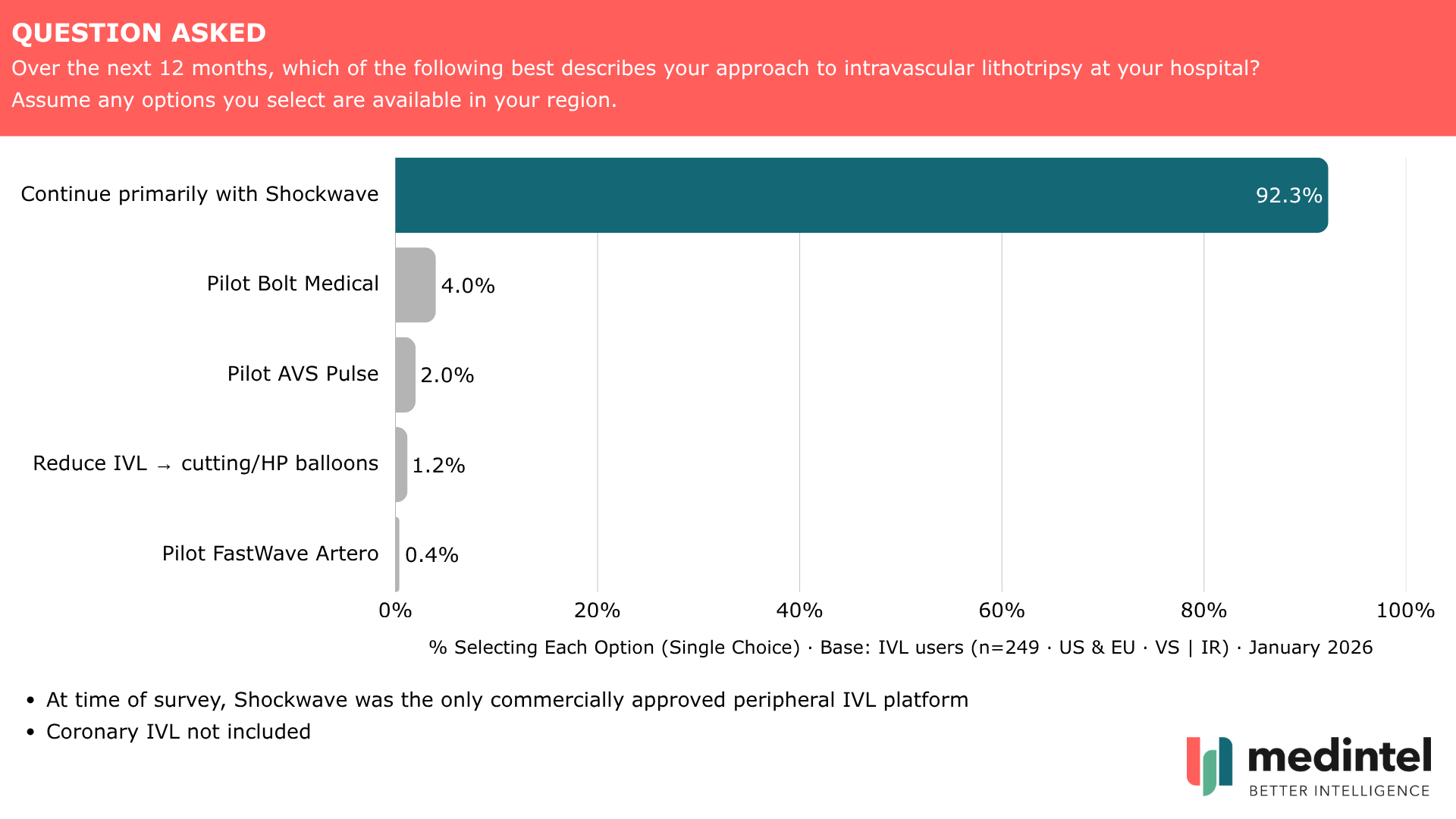

Adoption is already high. 80% of vascular surgeons and interventional radiologists already use IVL. At the time of survey, Shockwave was the only commercially approved platform in routine peripheral use. We asked IVL users how they expected to adapt their practice as new systems entered the market (n=249). 92% planned to continue primarily with Shockwave. Bolt Medical — now Boston Scientific Seismiq — had 4% pilot intent. AVS had 2%. FastWave under 1%.

"The 92% figure tells you everything about why challengers need a Stryker or Boston Scientific behind them," says Kilian Toal, Partner at medintel. "You don't move procedural share at that level of entrenchment through clinical evidence alone."

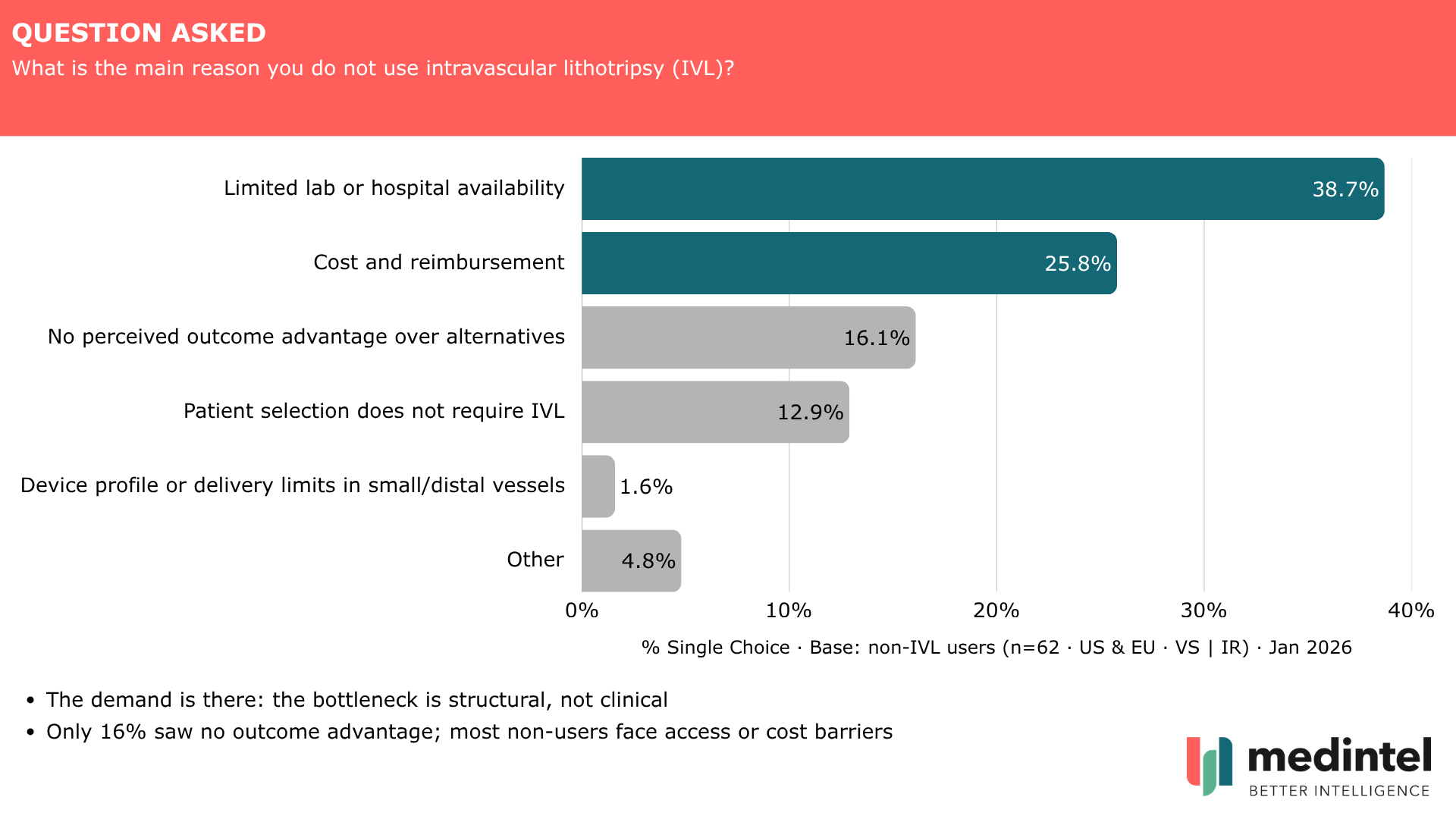

Among the 20% not currently using IVL (n=62), 39% cited limited lab or hospital availability as the primary barrier and 26% cited cost and reimbursement. Only 16% saw no outcome advantage over alternatives. A further 13% indicated their patient caseload simply doesn't require it: a reminder that non-use isn't always a conversion opportunity.

The demand is there. The bottleneck is structural — and new 2026 CMS peripheral IVL add-on codes, effective January 1, directly address part of it.

One finding rarely captured in public commentary: 59% of physicians surveyed also use IVL in aortic and iliac procedures for endograft delivery and sealing in EVAR not just in peripheral.

These findings are consistent with our September 2025 survey of 162 vascular surgeons and IRs across the US and EU, in which 33% named IVL as the PAD technology they were most excited about over the next three years — more than double the interest in absorbable stents, atherectomy, or drug-eluting technologies.

A note on scope — and what comes next

Both surveys were limited to vascular surgeons and interventional radiologists. This was a deliberate methodological choice, but it carries an important implication: in the US, interventional cardiologists perform a significant volume of peripheral vascular work, and in markets like Germany, angiologists contribute meaningfully to peripheral IVL practice. Neither group is captured here. Our peripheral adoption figures are therefore likely to understate true market penetration rather than overstate it.

This gap is something we intend to address. medintel is planning a dedicated IVL survey in the interventional cardiology space — covering both peripheral practice and coronary use — in the coming months.

On coronary IVL

This research covers peripheral and aortic practice only. The coronary space is a separate, large market moving fast — Abbott completed TECTONIC enrollment in April 2026, FRACTURE data is due in 2H 2026, and EuroPCR 2026 this month includes a dedicated late-breaking session featuring ICARE (IVL vs rotational atherectomy at 12 months) and FRACTURE interim data. It is also worth noting that ShortCUT and VICTORY (TCT 2025) showed cutting balloons and super-high-pressure NCBs to be non-inferior to Shockwave on minimal stent area in moderate calcification — prompting some ACC commentary repositioning IVL as a tool for genuinely recalcitrant calcium rather than a default. medintel will cover coronary IVL separately.

ENDS.

NOTES:

* Shockwave grew 18.5% year on year in Q1 2026 to $305 million and is launching fifth-generation coronary and peripheral catheters this year. Boston Scientific Seismiq is in US limited market release with FRACTURE coronary trial data expected in 2H 2026. Stryker expects the AVS deal to close in Q2 2026 with potential Pulse IVL FDA clearance before year-end. FastWave is preparing to start its Artero peripheral pivotal trial. The peripheral IVL space is moving from a one-player market to a four-way race within 12 to 18 months.

January 2026 survey: n=311 vascular surgeons and interventional radiologists, US and EU. September 2025 survey: n=162, same specialties and geographies. Both independent and non-commissioned, conducted via the Mr Doctor Network panel. Peripheral and aortic practice only. Interventional cardiologists not included.

For the underlying data: intel@medintel.co.uk